By Guest Author Insider Monkey. It’s widely

assumed that Warren Buffett doesn’t invest in technology stocks, but in recent

years, this belief has contrasted with reality. After accounting for zero

percent of his equity portfolio at the end of 2010, the tech sector now makes

up one sixth of Buffett’s stock holdings. At Insider Monkey, we’ve discovered

that hedge funds and other prominent investors’ best stock picks exhibit market-beating potential, so it’s worth paying attention to these

developments.

In the case of

Buffett and Berkshire Hathaway, they're not your typical technology investors. They

follow a very strict set of rules when selecting investments in this space,

which, through our observations, boil down to finding tech companies that: (1) trade

at very cheap multiples, (2) pay a

dividend, and (3) have sustainable product offerings that will safeguard their

survival over the next 15 to 20 years.

With this in mind,

the next logical question in many Buffettologists’ minds is: will the Oracle

buy shares of Twitter [TWTR] once it becomes a publicly traded entity?

This was the same

question many Facebook [FB] enthusiasts asked after its IPO last year and to

no surprise, many mega-investors bought in. Buffett didn’t, however, and it is

evident that Facebook broke all three of the rules described above. The stock traded

at more than 70 times earnings upon going public and there simply wasn’t any

assurance that it wouldn’t go the route of MySpace, Digg, Xanga and the rest of

social media’s fallen giants. It also didn’t offer a dividend, and still

doesn’t to this day.

Twitter faces all

three of the same problems.

According to most estimates,

Twitter will be valued near $11 billion when it goes public, giving it a per

share value between $19 and $20. At this price, the company will theoretically

trade at about 18.3 times this year’s estimated revenue, which most

conservative analysts expect to be around $600 million.

Facebook,

meanwhile, is valued at a price-to-sales multiple near this mark, while

LinkedIn [LNKD] is also in the same vicinity. It’s unreasonable to expect that

Buffett would be attracted to a valuation in this range if he hasn’t been

before.

Equally as

important, we also expect that the billionaire will take issue with Twitter’s

outlook over the next 15 to 20 years. While some may argue that the micro

blogging service can generate more advertising revenue than a Facebook or a

LinkedIn for example, there’s still no guarantee that Twitter will be around in

two decades. Obviously, there’s no such thing as 100% certainty in any

industry, but there are fewer risks facing Buffett’s favorite investments, like

Wells Fargo [WFC] and Coca Cola [KO], than there are to any social media company.

Putting the final nail

in the proverbial coffin, we also know that from Twitter’s S-1 filing, it has no plans to declare dividends “in the

foreseeable future.”

So, if Warren Buffett

won’t buy Twitter, what stock is responsible for the majority of his investment

in the tech sector?

As reported in his

latest 13F filing, the answer is IBM [IBM]. Buffett and Berkshire

hold almost 15% of their $89 billion equity portfolio in the information

technology giant, and it meets all three of our aforementioned criteria. IBM

trades at a mere 9.9 times forward earnings, has five diversified business

segments from IT infrastructure to software, and it pays a dividend yield above

2%.

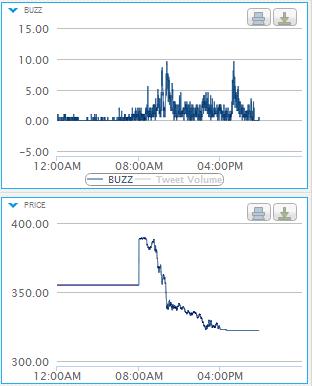

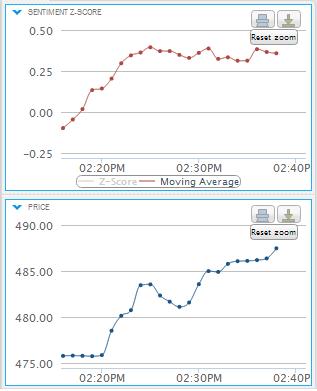

The market has seen a bad

performance over the year. First a solid gain and than a sharp sell-off. What matters

now is the Fed rate hike.

The market has seen a bad

performance over the year. First a solid gain and than a sharp sell-off. What matters

now is the Fed rate hike.

{kind=link}

{kind=link}

{kind=link}

{kind=link}